You already have a strong desire to become a homeowner, and you will achieve it by doing your part in a process that will transform your financial life!

Become a homeowner is a significant milestone for everyone. It will bring you a sense of pride, stability, and, most importantly, the opportunity to create wealth.

However, homeownership can be overwhelming, especially if you are a first-time buyer who needs help figuring out where to start.

In this post, I’ll guide you through how to become a homeowner, from improving your financial profile, getting approved for a home loan, and finding and working with your real estate agent until you get the keys to your home.

For most people, buying a home is only possible through financing, so working on your creditworthiness is critical to reaching homeownership.

Who is a First-Time Home Buyer?

From a lending standpoint, a first-time buyer is any person who has not owned a piece of real estate in the last three years, even though they could own one or more properties in the past that were sold or foreclosed, and who is planning to use the property as a primary residence.

Here in the United States we have the FHA mortgage loans that promote homeownership offering to the first-time buyers better loan conditions compared with the conventional mortgage loans, particularly in the following areas:

- Low Down-Payment

- Low Closing Costs

- Easy Credit Qualification

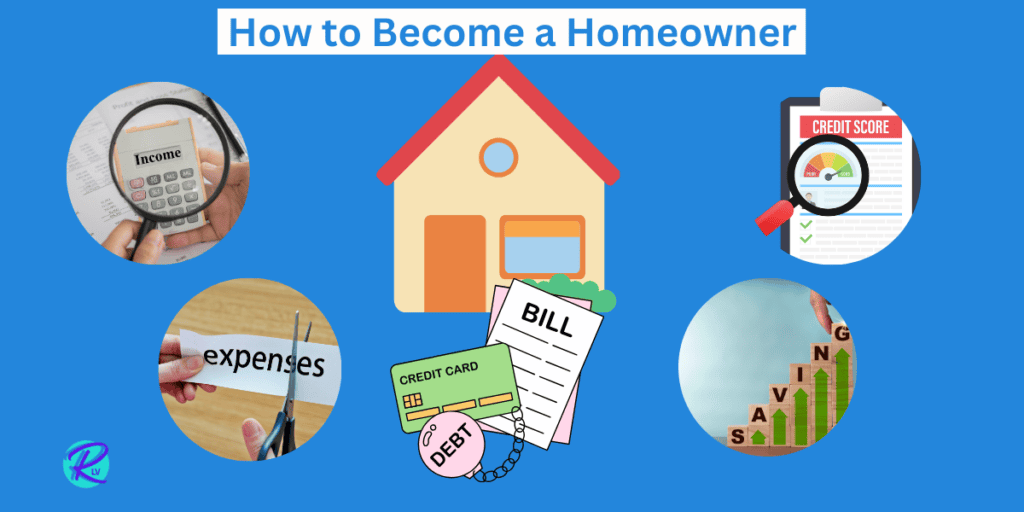

Understanding your Finances

How to become a homeowner is in knowing your income, expenses, debts, savings, and credit score because all of them combined ultimately define your creditworthiness when seeking financing.

Before applying for a home loan, review all of the elements of your financial profile, and optimize how you handle your income, expenses, debts, and savings. After that, you will show and prove that you are a qualified borrower in the eyes of the mortgage lender who will lend you money to become a homeowner.

Doing that may be easy for some, but there is resistance among many people to see the truth of the numbers. Being in a situation where you must confront a relationship with money is not a delightful task. Still, if you are clear about your goal of becoming a homeowner as a solid foundation to build financial independence, you are sure you will overcome those fears.

Income and Expenses- BUDGETING

The general rule is that your monthly housing expenses should be no more than 30% of your gross monthly income to be considered affordable. But that’s optimistic. Besides the mortgage loan, there are other housing expenses to consider: property taxes, homeowners insurance, Homeowners associations, HOA, and utilities.

According to the FHA guidelines, a debt-to-income ratio over 46% of the gross income disqualified any prospective buyer for an FHA loan.

The first and simple thing you should do is figure out your monthly and yearly net income. You will be surprised of what actually hits your bank account after taxes, insurance, and all those other little deductions. Take that number and then start listing out all your monthly expenses. And I mean everything—not just rent and utilities, but also your Starbucks habit, streaming subscriptions, and that impulse to buy on Amazon. It all adds up.

By tracking your income and expenses, you create a budget, and then you can identify areas to cut back on.

Cutting unnecessary expenses will help you save money for your down payment and other homebuying paid upfront costs, diminish your financial obligations, and improve your financial profile.

Additionally, if needed, consider increasing your income with some side hustles. You can have many sources of income, but to get a pre-approval loan, you must show job evidence of at least two years in the same line of work.

Savings

Saving for a down payment and other homebuying expenses, like closing costs, is one of the biggest hurdles to homeownership.

In addition to cutting back on discretionary expenses and earning more money through a side hustle, consider setting up automatic savings contributions.

If possible, save 20% of the market’s home value as a down payment to apply for a conventional loan, avoiding private mortgage insurance (PMI).

Assuming you are a first-time buyer, the FHA mortgage loan requires as little as 3.5% down.

Your Credit Score

The FICO score is the ranking of your creditworthiness. It is a number from 350 to 850 that scores your history of credits and your habits to paying them. The higher the credit score, the better, as you can secure favorable interest rates for the life of the home loan, saving you many thousands of dollars.

Equifax, Experian, and TransUnion are the three major credit bureaus, and you can request an annual free copy of your credit report.

Carefully review it, and if it is pertinent, clarify any inaccuracy or mistakes with them before applying for a mortgage.

If your score isn’t where it needs to be, take some time to improve it before diving into the homebuying process. Pay down credit card debt, make sure you’re paying bills on time, and pay the credit card balance every month if possible.

Avoid opening new credit accounts if you can, and if you pay any line of credit in full, do not close them either.

Getting a handle on your financial situation could be one of the most challenging parts of homebuying. Still, at the same time, it would be the most rewarding as you start having financial awareness, which at the end will helps to take the actions to generate more income, define a budget for your expenses and savings, and improve your credit qualification.

Debts

It’s crucial to evaluate your debt-to-income ratio.

It is the amount of debt you have compared to your income. Most mortgage lenders prefer a debt-to-income ratio of 36% or less. If you have a lot of credit, consider paying it down or eliminating it before applying for a mortgage. As I mentioned before, if you apply for an FHA mortgage loan, having a debt-to-income ratio below 46%-43% is an excellent place to start. The lower the ratio, the better.

Get Pre-Approved for a Home Loan

This process involves evaluating your financial information with a mortgage lender to determine how much they are willing to lend you and what your mortgage options are.

The pre-approval can help you narrow the home search price and give you an idea of your monthly mortgage payment.

To get pre-approved, you’ll need to gather some important documents, such as pay stubs, tax returns, and bank statements. You’ll also need to provide information about your credit history and employment status.

The pre-approved letter is the beginning of the process of becoming a homeowner. Now, you need to find a realtor to represent you in buying the home you can afford.

Do Not Risk your Pre-Approval

As a Realtor, I’ve had the experience of working with a prospective buyer who had an excellent pre-approval letter from a lender, good enough to start looking for homes.

They found the home they loved, so they made an offer. During the contingency period, the lender confirmed they weren’t qualified to buy that property. What happened? After getting the pre-approval, they got another loan that left them without room for a mortgage loan.

Unable to repay the loan, they canceled the transaction, and I clearly remember their frustration for not getting the home they loved. In buying a home, communication with your realtor and lender is critical.

So, don’t sabotage yourself! After getting the pre-approval letter, avoid any action that can affect your credit score and debt and income ratios, like getting another loan, making big purchases financed with a credit card, or co-signing for somebody.

Find Your Realtor

Working with a realtor will ensure a smoother and less stressful homebuying journey by providing you with full representation.

Find a reputable realtor by requesting referrals from friends and family or checking online reviews.

According to the Nevada Division of Real Estate in the Las Vegas area, in July 2024, there are more than 15,741 active agents, 2,186 brokers-salespersons, and 1,859 brokers.

In a buyer consultation meeting, an agent will explain the home-buying process, and provide the details of the offered representation services. The Realtor will help you find homes that fit your budget and needs, provide valuable insights into the local market, and negotiate the purchase agreement on your behalf.

Be Aware of the Buyer’s Commission New Rule.

According to the recent NAR settlement, starting August 17, 2024, before starting to tour homes, you and your agent need to sign a written agreement called a Buyer Representation Agreement. This agreement includes the terms of the services the agent will perform, for how much, and for how long. This buyer agreement also applies to virtual home tours.

Keep in mind that the buyer’s agent commission is always negotiable.

Once you’ve found the agent you’re comfortable working with and signed the BBRA, you can start visiting homes. The agent will provide property listings that fit your criteria, arrange home tours, and guide you through the negotiation and closing process.

House Hunting

House hunting could be the most fun part of homebuying if you have a clear list of must-haves and nice-to-haves.

Think about your lifestyle and what you really need. Write your list down, rank each item, and share it with your agent. It will help stay focused when looking at different properties.

Location is everything. You can change almost anything about a house, but you can’t pick it up and move it to another neighborhood or city in the metro area of Las Vegas.

Spend time researching neighborhoods—checking out schools, hospitals, public libraries, and local amenities, and even driving around at different times of the day to get a feel for the area.

Another tip: stay focused on cosmetic issues. It’s easy to walk into a house and be turned off by ugly wallpaper or outdated fixtures, but those things are relatively easy and inexpensive to change.. It’s essential to focus on the bones of the house, the layout, the structure, and the things that are harder to change.

However, don’t ignore red flags. Trust your gut if something doesn’t feel right, and ask questions.

One last thing—Take your time, take notes, and don’t be afraid to say no if something doesn’t feel right. Your HOME is out there, but you might need to kiss a few frogs along the way.

Make an offer and negotiate.

When you find the home that fits your needs and budget, it’s time to make an offer.

Making an offer is when things get real. The first step is figuring out how much to offer.

At this point, the agent’s expertise came in handy. Your agent will run a comparative market analysis (CMA), which compares the home you are interested in with similar homes recently sold in the area. It gives you a good idea of what the house is worth and what a fair offer would be.

But it’s not just about offering the right amount—timing and other factors come into play, too. For example, if the house has been on the market for a while, the seller might be more willing to negotiate. On the flip side, if multiple offers are on the table, you might need to come in strong to stand out.

The offer isn’t just about the price. Other elements, like contingencies, can make or break a deal.

Your realtor will draft an offer that includes the price, contingencies, and other terms of the sale. Considering the new buyer’s agent compensation rule, the offer can include a request for the seller to pay your agent’s commission as other concessions like your closing costs.

When you receive a counter from the seller regarding your initial offer, it indicates that there is room for negotiations.

Get a home inspection and appraisal.

A contingency is basically a condition that must happen for the sale to go through. The most common are loan approval, home inspections, and appraisal contingencies.

Assuming that getting the loan will be fine because you disclosed everything related to your credit and finances to the loan officer, getting a home inspection and appraisal is vital during the property sale.

Regarding home inspections and appraisals, I can’t stress enough how necessary these steps are in homebuying. They differ between buying your dream home and entering a financial nightmare. Both inspections allows further negotiations on price and repairs.

Home Inspection.

A home inspection is a deep dive into the health of the house you’re about to buy, and you will receive a detailed report of the condition of the central systems in the house, roof, plumbing, electrical, and appliances.

The last thing you want is to move in and then find out you need to replace the entire HVAC system. That’s why I always advise my clients to attend the inspection themselves. I know it might sound tedious, but being there gives you a firsthand look at potential issues, and you can ask the inspector questions on the spot.

In Southern Nevada, you pay the inspection cost to the selected inspector upfront.

Appraisals.

Appraisals are all about value. Even if you and the seller agree on a price, the lender wants to ensure the house is worth your pay. A professional appraiser evaluates the property’s worth based on recent comparable sales in the area, location, and home’s condition.

The appraisal is another item buyers usually pay upfront. Some lenders include the assessment cost in the lending costs at the transaction’s closing.

Inspections and appraisals aren’t just formalities—they’re your best friends in this process. They protect you from overpaying and help you avoid unexpected repair costs after you’ve moved in. Always take them seriously, and don’t be afraid to negotiate based on what you find in the home inspection and appraisal report. It might feel like a lot of back-and-forth, but it’s all part of ensuring you get a fair deal.

Once you’ve completed the negotiation process based on the home inspection and the appraisal, and your lender is ready to fund the loan, it’s time to prepare for the closing day.

Closing the purchase of your home

Closing the deal is the moment when everything comes together. It would help if you did a few things in those final days leading up to closing. It’s exciting and nerve-wracking, but trust me, it can go smoothly with the proper preparation.

Two or three days before the closing, you can do the final walk-through to ensure the house is in the expected condition and that the seller has completed all agreed-upon repairs, if applicable, before you sign those final papers.

Also a few days before the closing date you will get a document called a Closing Statement, which outlines all the final numbers under your responsibility, like the balance of the down payment, closing cost and any amount of your agent commission to your agent that wasn’t pay by the seller according to the negotiation of the offer you presented. The closing statement also specifies how much cash you must transfer to the escrow company before the closing day.

On the closing day itself, be prepared for a mountain of paperwork. You’ll be signing documents that cover everything from the mortgage note to the deed of trust. It’s a lot but take your time. If there’s anything you need help understanding, ask for clarification. It’s your right; knowing what you’re committing to is essential.

On closing day, Finally, once all the documents are signed, the funds are in the escrow account, and the deed with your name on it is at the Clark County Recorder Office, you’ll get the keys to your new home. That moment—when they hand you the keys—is really amazing.

After all the hard work, stress, and waiting, it paid off immediately. You’re officially a homeowner!

MOVING INTO YOUR NEW HOME

Almost there! After finding the right place, securing financing, and closing the deal, it’s finally time to make that house your home. But before you can kick back and relax, there are a few essential steps to ensure a smooth transition. Here’s a list of what to focus on when moving into your new home.

Planning Your Move and Hiring Movers: One of the first things you’ll want to do is plan your move well in advance.

Setting Up Utilities and Services: Once the move is under control, set up utilities and services at your new home. Ideally, it would help if you transfer or activate utilities like electricity, water, gas, and internet before moving day. Here in the Las Vegas metro area, it is customary for sellers to give the buyer a courtesy of two to three days after the closing to change the utilities, electricity, and water under your name.

Tips for Making Your New House Feel Like Home: Start with the rooms you’ll use the most, like the bedroom, bathroom, and kitchen, to get settled quickly, and feel on your own

Joining Your New Community: Remember to introduce yourself to your new neighbors and get involved.

Moving into a your home is both an end and a beginning. Patience and planning help you have a smooth and enjoyable transition, setting the stage for many happy years ahead in your new place.

Final Words

Congratulations on embarking on the journey to become a homeowner in Las Vegas! By following this step-by-step guide, you have a clear roadmap to find the perfect home for you and start creating not only wealth but a solid future for you and your family. Welcome to homeownership!