Homeownership is an effective proven way to build wealth in real estate to achieve financial success. You can reap its great long-term benefits!

Investing in your home instead of renting gives you a solid foundation for your financial future. You are solving the need for shelter and acquiring a tangible asset, which is critical for creating wealth.

Despite current economic challenges, owning a home is achievable and offers numerous financial and non-financial benefits that outweigh any obstacles.

Taking control of your financial profile and improving it as much as possible will open the door for financing opportunities. Don’t underestimate the financial advantages of being a reliable borrower.

Let’s look more in detail at the financial benefits of homeownership to help you build wealth and how you might prepare to reach it.

Definition of Homeownership

Homeownership refers to the legal rights of ownership and possession of a property to use as a primary residence. It involves acquiring, maintaining, and managing residential properties such as homes, condos, and apartments.

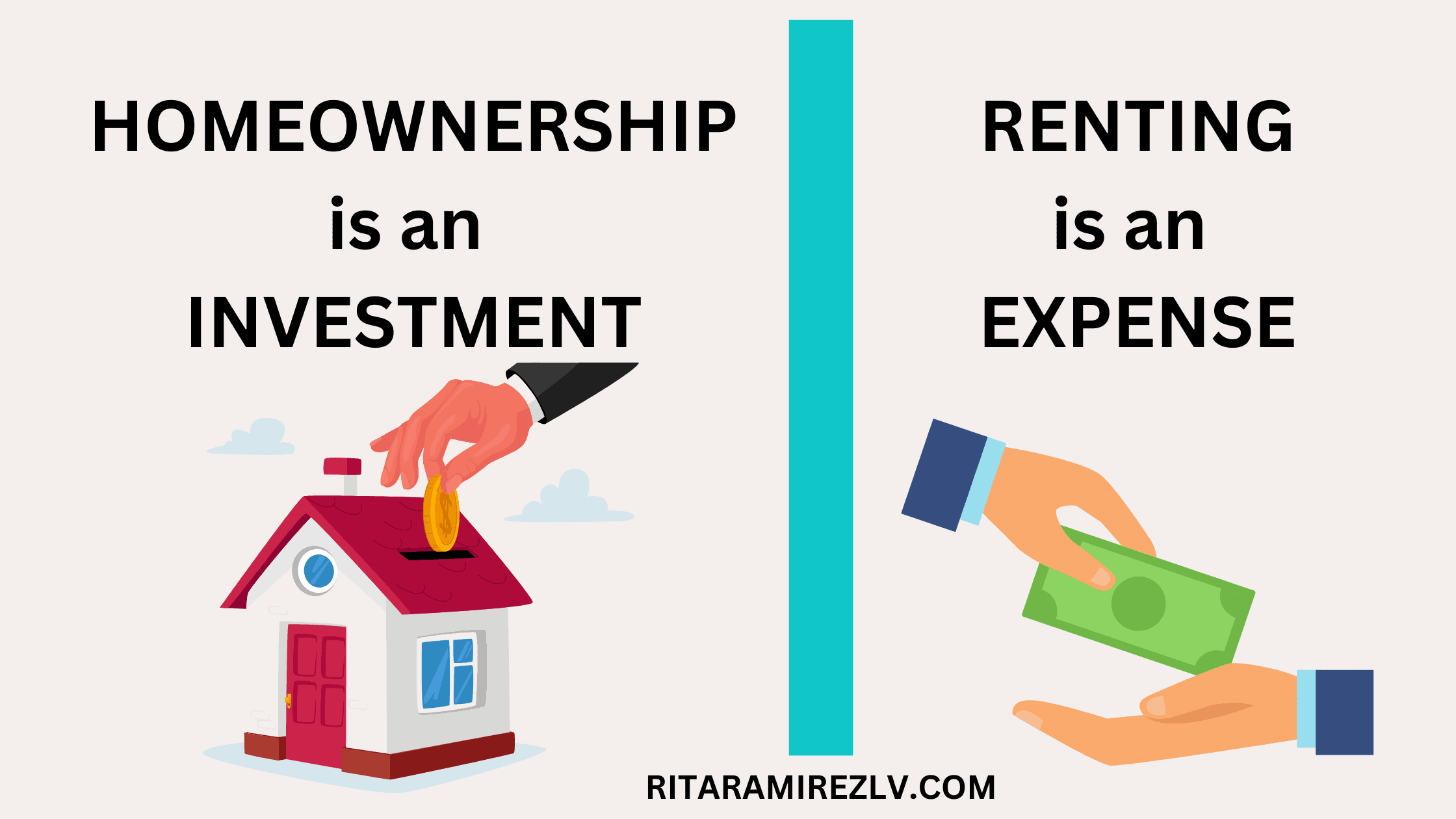

Buying or Renting?

Homeownership is an investment while renting is an expense. What buying and renting have in common is that either one provides shelter.

Homeownership has long been a cornerstone of wealth building in America, with numerous advantages over renting. Sadly, fewer people can purchase homes nowadays, leaving many families with renting as their only option for housing.

The 2022 Survey of Consumer Finances (SCF) from the Board of Governors of the Federal Reserve, adjusted for inflation to 2022 dollars, reveals significant financial disparities between homeowners and renters in the United States. Homeowners have a median annual income of $94,040 before taxes, compared to $42,160 for renters. Moreover, the median net worth of homeowners is $396,500, which is a stark contrast to renters’ net worth of $10,410. It simply means that in the United States a homeowner has a net worth 38 times bigger than the net worth of a renter. This wealth gap between homeowners and renters will only widen, making it more difficult to narrow it.

However, by embarking yourself in the journey of preparing to become a homeowner and reaching that milestone, you could transform the trajectory of your personal and family finances story.

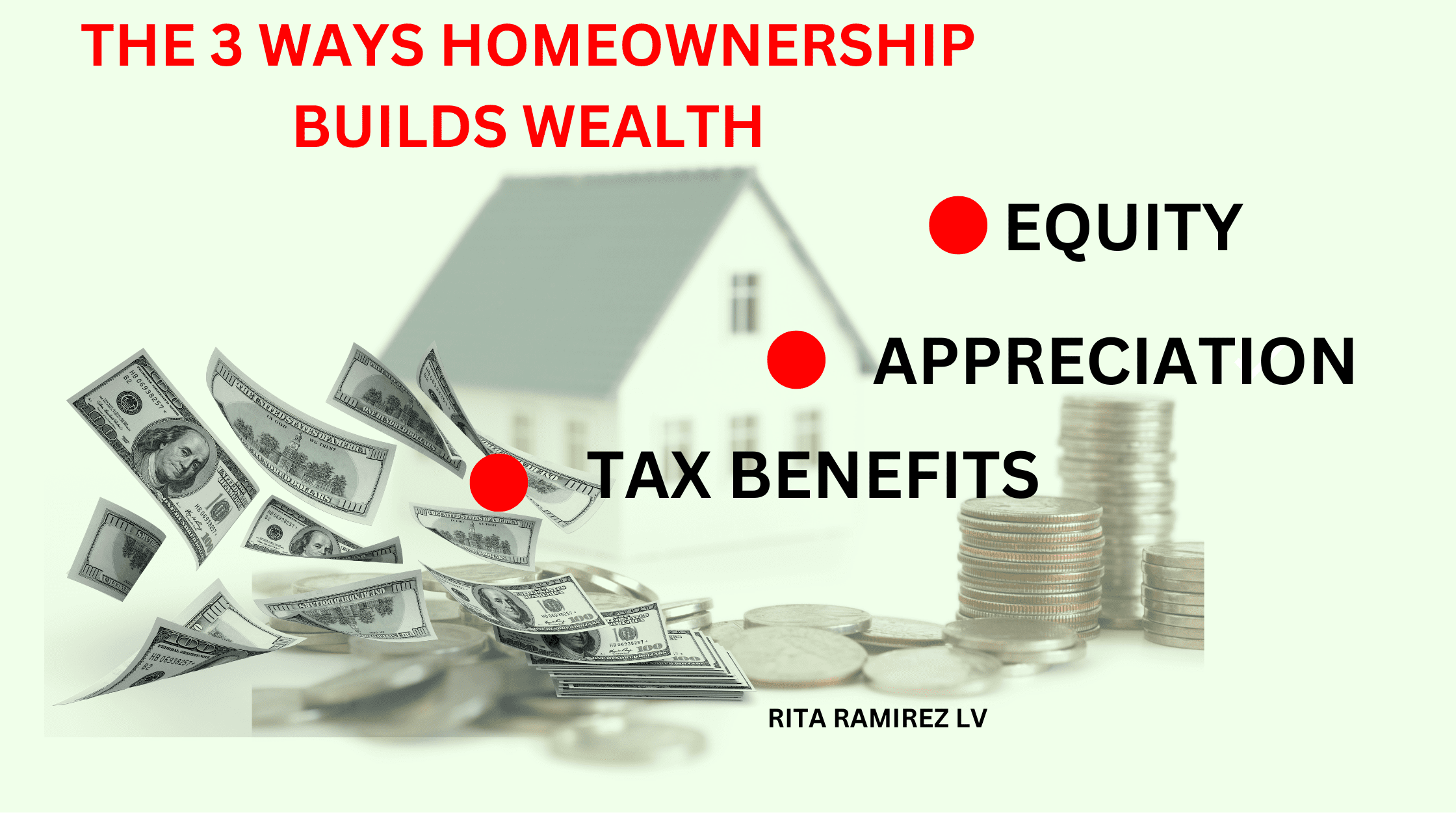

The Three Main Financial Ways Homeownership Builds Wealth.

Home Equity

Home equity is the amount you own over your home!

Here we are discussing how you build equity by paying the mortgage bill of the loan that allowed you to become a homeowner.

Let’s say you are buying a home for $350,000, putting 3.5% of the purchase price as your down payment, $12,250, and financing the rest, $337,750, at an annual interest of 6.94%, which is the national average 30 years fixed mortgage reported by Fanny Mae on Thursday, May 23 of 2024.

A loan table amortization shows that the fixed monthly bill will be $2,233.47 for the life of the loan. For the first month of the loan, $280.14 go to the principal, and $1,953.32 go to interest.

During the first years of the loan, the amount that goes to the Principal is small but grows over time as you owe less, and the amount for interest decreases.

Fixed Monthly Payment= Principal + Interest

For illustration purposes, we are not including other costs in an actual mortgage bill, like private mortgage insurance, PMI, property taxes, and home insurance.

When adding all payments applied to the principal at the end of every year from 1 to 10, in this example, you have an idea of your equity gains as follows:

| Year | Principal Paid | Interest Paid |

|---|---|---|

| 1 | $3,470.76 | $23,330.83 |

| 2 | $3,719.44 | $23,082.15 |

| 3 | $3,985.94 | $22,815.65 |

| 4 | $4,271.54 | $22,530.05 |

| 5 | $4,577.59 | $22,223.99 |

| 6 | $4,905.58 | $21,896.01 |

| 7 | $5,257.07 | $21,544.52 |

| 8 | $5,633.74 | $21,167.85 |

| 9 | $6,037.40 | $20,764.19 |

| 10 | $6,469.99 | $20,331.60 |

See how it works?

Over time you own more of your house and owe less on loans. Then, your net worth is growing while enjoying the long-term benefits of homeownership.

If you were renting, all the monthly rent goes directly to help your landlord to build more equity if he is using financing or a total return on their investment if they are free of debt.

Home Appreciation

Home appreciation is the increase in the value of a property over time

According to the National Association of Realtors, NAR, during the last decade, middle-income homeowners gained more than $120,000 in wealth, from home appreciation.

Positive changes in the value of your home are due mainly, to the following:

- Real estate market changes, as experienced during the pandemic when home values skyrocketed, due to a high demand for houses, and a low inventory. In the south of Nevada, according to LVR, the median price for homes sold went from $319,000 in March 2020 to $363,00 in March 2021. A staggering median annual price increase of 13%. Normal market conditions still increase the housing market by about 3% to 5 % annually. In July 2024, Las Vegas’ median home sales price rose to $480,000, an increase of 13.6% over the national median price of $422.600.

- Make improvements to your home, like renovating the kitchen and baths or adding another room or a bath.

When property appreciation happens, your home becomes more valuable, your net worth increases, and the future price to sell it, too.

Tax Benefits

The tax law foresaw several benefits for the owner of a property, including tax deductions for the following concepts:

- Mortgage interest. One of the most commonly known tax benefits. The interest paid on their mortgage, is a tax deduction, which can be a significant amount during the early years of a mortgage.

- Private mortgage insurance (PMI). Some homeowners can deduct the premiums they pay for private mortgage insurance if they didn’t put down at least 20% when purchasing their home. However, the deductibility can phase out at higher income levels.

- Mortgage points. If you paid points to get a more favorable interest rate on your home purchase or refinance, you can deduct those points in the year you paid them.

- Property taxes. Homeowners can also deduct the amount they pay in property taxes every year.

- Capital Gains Exclusion: You can exclude up to $250,000 of the profit gains when you sell your home, if you are single, and up to $500,000 if you are married.

- Home Office Deduction: If a portion of your home is used exclusively for business purposes, you may qualify for a home office deduction. You can deduct a percentage of your home office’s expenses, such as mortgage interest, property taxes, utilities, repairs, and depreciation, based on the proportion of your home used for business.

- Energy-Efficient Home Improvement Tax Credits: Homeowners who install energy-efficient systems or renewable energy systems, such as solar panels or geothermal heat pumps, may qualify for federal tax credits. Potential tax credits for energy-efficient windows, doors, or insulation exist.

- Rental Income: when you rent out a section of your home, you must report the rental income, but you can also deduct related expenses, including depreciation, utilities, insurance, and others.

- Casualty and Theft Losses: If your home suffers damage or loss due to a sudden event like a natural disaster or theft, you can deduct some of the losses not covered by insurance.

- Home Accessibility Tax Breaks: Elderly or disabled homeowners who modify their homes for medical reasons may be eligible for tax deductions. Improvements like wheelchair ramps, grab bars, and other accessibility features can deducted as medical expenses.

- State and Local Benefits: On top of federal benefits, many states also offer tax credits, deductions, or rebates for homeowners. It’s essential to check your state’s tax laws and incentives, especially regarding energy-efficient home improvements.

Always is important to consult a tax professional who will advise you on your best option, if is better for you to itemize your taxes or take the standard deduction.

Other Financial Benefits of Homeownership

From increasing your financial leverage to stabilizing your housing expenses and providing potential sources of income, homeownership is a smart financial decision that will benefit you in the long run.

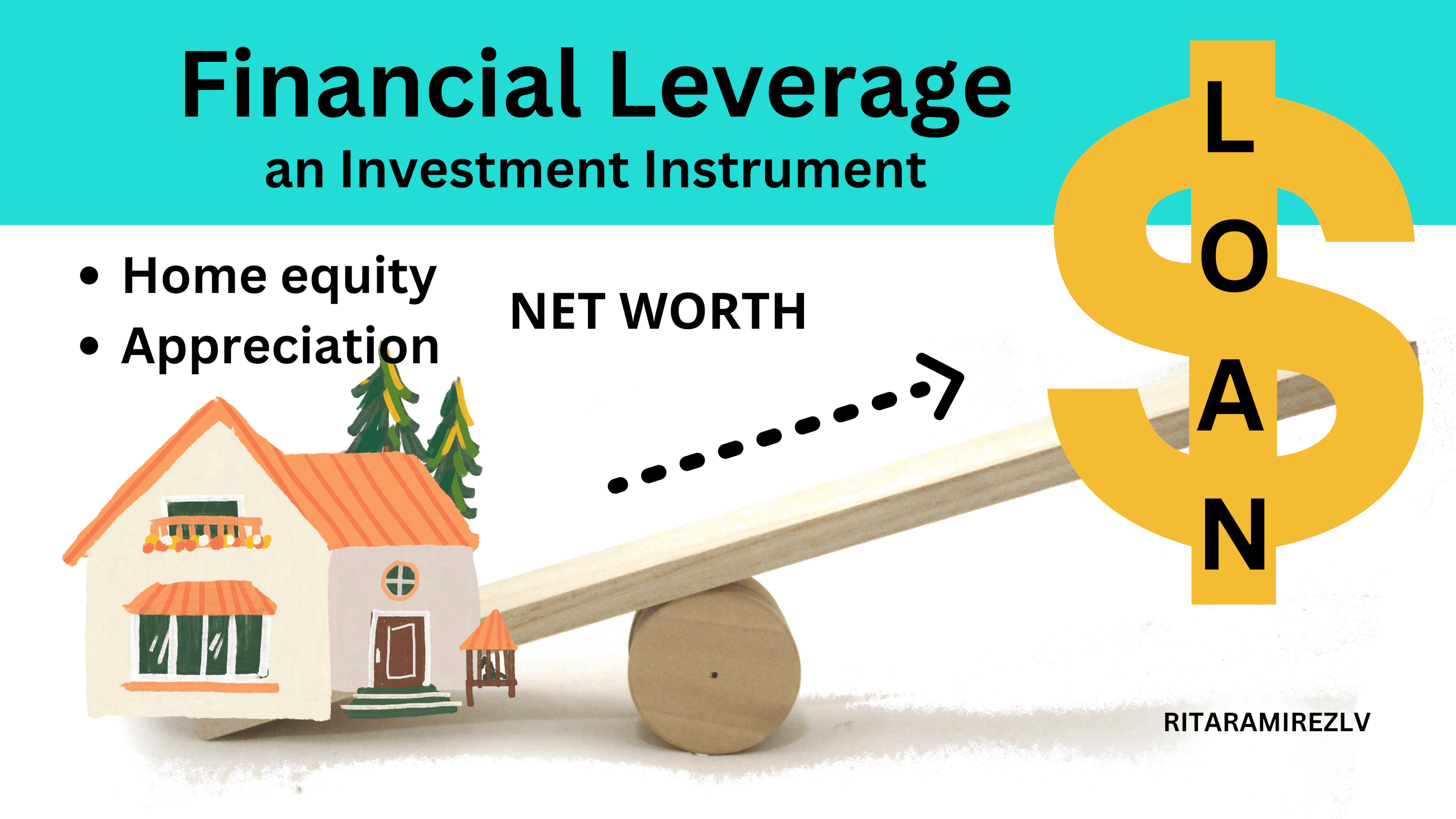

Increase Your Financial Leverage

Owning a home enhances your financial leverage, a valuable investment instrument for wealth building.

Your net worth has increased since you became a homeowner. You have more equity every month and earn some property appreciation.

All of that make you a more solid borrower, able to get better interest rates and loan conditions. That is financial leverage.

You can apply financial leverage to build wealth by getting a loan using your house as collateral. Then you can purchase another asset, such as your first rental property, or pursue other real estate business ideas to generate additional income.

Financial leverage has been the magic formula used for centuries for wealth creation starting with homeownership.

You can repeat the process as much as possible and grow as a real estate investor.

With a word of caution here, you should use this strategy carefully because you don’t want to have more debt than you can handle without putting all your plans at risk.

Keeping Housing Expenses Under your Control

When you are a tenant, your landlord can increase your rent at the end of each lease term, which can be unpredictable and potentially disrupt your budget. However, as a homeowner, you can take advantage of a fixed-rate mortgage, which provides certainty and stability in your housing expenses. It allows you to plan your budget better and avoid unexpected increases in your housing expenses.

A Potential Source of Income

When you own a home you become the owner of an asset, which mean it holds value and has the ability to generate income. As a homeowner you have the opportunity to renting out a room or part of your property to generate additional earnings. It can help you repay your mortgage faster, grow your savings, or pursue other investment opportunities.

First Things to Do to Reach Homeownership

Assuming that you are like most Americans that need financing to buy a home, being eligible for a loan is one of the most crucial things you will do once you set your mind on homeownership.

Financing the home’s purchase price with a mortgage loan is the typical method to access homeownership. Buyer contribution goes from 3% to 20% of the purchase price as a down payment.

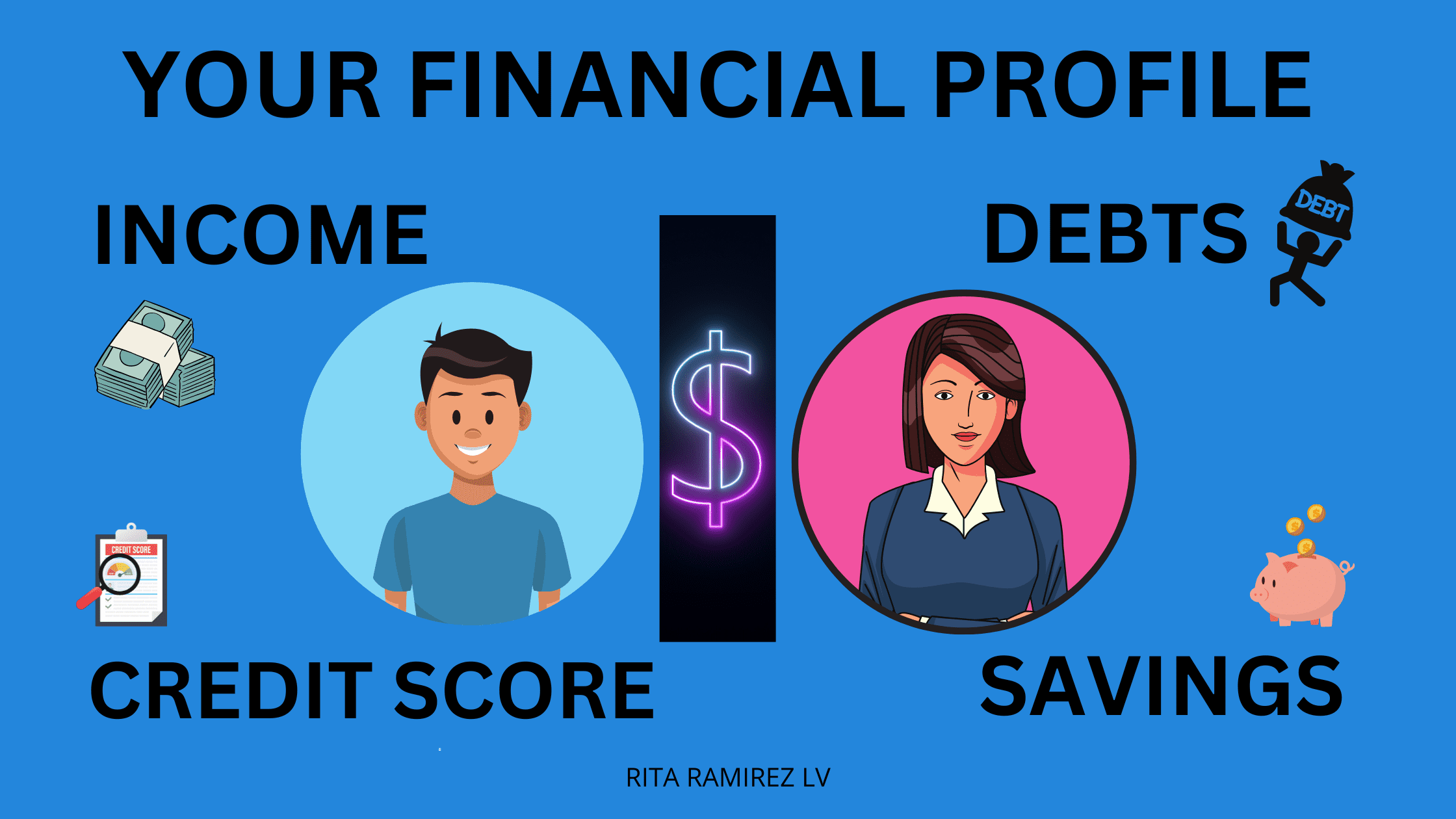

Work on Your Financial Profile.

To get the financing, putting your finances in order is one of the most critical steps when preparing to reach homeownership.

Consider raising your monthly earnings, controlling your monthly expenses, reducing your debt obligations, clarifying any errors in your credit report, also known as FICO, and saving as much as possible.

Additionally, make available the documents to support it, like the following:

- Steady source of Income from at least two last years in the same line of work.

- Proof of employment.

- Credit score. You can obtain an annual free copy of your credit records.

- Tax returns.

- Financial statements to show funds availability to cover the down payment and closing costs.

Get Pre-Approved for a Loan.

Based on your financial profile, the lender determines how much home you can afford.

The mortgage lender has reviewed your financial profile and determined what amount of money they will lend you and which home loan program fits better for you. You are Pre-approved!

Getting pre-approved for a mortgage loan is a milestone in homeownership. It is an accomplishment. You are creditworthy, and you should be very proud of yourself!

It also allows you to start shopping around for homes, shows sellers that you are serious about finding a home, and makes them more likely to accept your offer.

Conclusion

Homeownership is an investment that could be challenging, but you can achieve it with the right mindset and preparation. Make yourself eligible for a loan taking care of your finances. Getting pre-approved for a loan will give you the certainty that you can become a homeowner and the confidence to shop for houses with the guidance of your real estate agent. Choose homeownership to start building wealth in real estate!

![How to Become a Homeowner in Las Vegas [2024]](https://ritaramirezlv.com/wp-content/uploads/2023/04/How-to-Become-a-Homeowner.png)